Is there a level playing field in the Dutch market of Residential Mortgages?

To avoid cross-sector arbitrage, the European Commission has announced its intentions to “align” capital requirements for mortgages for insurers under the Solvency II regime with banks under the Basel III regime.

This article provides further background to this discussion and also shows that there are various business characteristics and principles underlying the regulatory capital frameworks that disrupt a level playing field between insurers and banks.

A pdf. of this article can be found by this link:

2022 Triple A – Risk Finance – Level Playing Field Residential Mortgages

Developments in the mortgage market

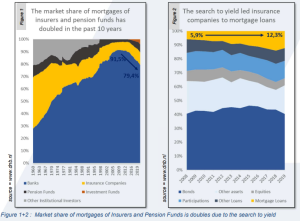

The share of banks in the Dutch mortgage market is declining

For more than 50 years, banks had an ever increasing share in the Dutch mortgage market. However over the past 10 years, the market share of banks has declined in favor of insurers (growth of 50% in past decade), pension funds (growth of 200% in past decade) and investment funds. See Figure 1.

The two main reasons for the changing developments in the mortgage market are the following:

- The low and flat yield curve. Long-term interest rates have fallen sharply in de past years. Because insurers and pension funds naturally have long-term obligations, it is more attractive for them than for banks to offer competitive mortgage interest rates. The search for yield has resulted in a doubling of the share of mortgages on the balance sheet of insurance companies. See Figure 2.

- The differences in capital requirements between mortgage providers. Over the past 10 years, there has been a trend that capital requirements for banks are (implicitly) increasing. Implicitly because the supervision of self-developed capital models at banks has been intensified which has led to all kinds of (imposed) capital add-on’s or more conservative models. Starting this year, the capital required for banks in the Netherlands increased even more (explicitly) because DNB has introduced a RWA[1] floor in the Netherlands, thereby raising the capital requirements for mortgages. The main reason for DNB to introduce this floor is the increased system risk caused by the developments in the Dutch housing market

[1] RWA = Risk Weighted Assets

Intention of EC to align prudential treatment of mortgages

Insurance companies have argued that alignment of capital requirements for mortgage loans between banks and insurance companies is not justified

During the past months, the European Commission (‘EC’) has announced the intention to amend the current prudential regulation of mortgage loans for insurance companies with the aim of aligning the calibration of the capital requirements for mortgages under Solvency II with the Basel (III/IV) credit risk framework of the banking sector. The EC’s stated aim is “to avoid any risk of cross-sector regulatory arbitrage”. The amendment on the treatment of mortgage loans under Solvency II was not included in EIOPA’s earlier published opinion on the 2020 review of Solvency II.

According to Insurance companies (represented by Insurance Europe), the EC’s stated intention to “align” the capital requirements is not justified based on different arguments. According to their view, the current treatment of mortgages under Solvency II is sound and there is no evidence that any amendment is needed. Clear and understandable arguments are put forward from insurers. A summary of key argumentation brought forward is shown in the table below.

In the remainder of this paper, the various items above are discussed in more detail on the basis of an elaboration on the capital requirements related to mortgages as well as actual results derived from public disclosures (pillar 3 reports / disclosures) from individual banks and insurance companies.

[2] Amortized cost value after allowance for Expected Credit Loss (ECL) where in case of impairment expected credit losses for the next year of the mortgage are considered unless credit risk increases significantly in which case ECL is calculated over the lifetime of the mortgage.

Further elaboration of capital requirement for credit risk exposure in mortgage loans

For a fair comparison of the capital requirements for banks, insurance companies and pension funds, further details are given below about the treatment of mortgage loans under the different relevant capital frameworks for (Dutch) financial institutions.

Banks (Basel III regime)

Under the Basel framework, the available capital (“total capital”) is predominantly derived based on IFRS carrying balance sheet values. The capital requirements are derived as the sum of market risk, credit risk and operational risk without taking diversification into account. Capital requirements are normally reflected in terms of Risk Weighted Assets, derived by multiplying the capital requirements for market risk, credit risk and operational risk by 12.5 (i.e. being the reciprocal of the minimum capital ratio of 8%). Since no diversification is allowed by banks between the risk types in their regulatory capital, the impact of an increase of capital related to credit risk has an 1 to 1 impact on the total capital required.

The credit risk related to mortgage loans is reflected in the credit risk capital requirement. Since the introduction of Basel II in 2006 banks have the opportunity to apply the Standardized Approach for their Capital Requirements or develop their Internal Models and use them to calculate the required capital. The requirements for Internal Models have become far more strict in the past 5 years to get or keep the “Advanced Internal Ratings Based (IRB) Approach” – status.

- Basel III Standardized Approach requires 4.38% capital for each mortgage with a Loan-To-Value with a maximum of 80%. For higher LTV’s the required capital grows gradually till 5.74% (LTV 110%) and more.

- Basel III “Finalizing Post Crisis Reforms” (or Basel IV) describes the new capital requirements that will become effective from 2025 onwards. There are two major changes in this context:

- The capital requirements for the Standardized Approach are changed. For mortgages with an LTV ≤ 75% the required capital will be lower (starting at 2.50%), for mortgages with an LTV > 75% the required capital will be higher.

- Internal Models become less attractive, since the capital requirement resulting from internal models will be exposed to a floor based on the Standardized Approach (for all portfolios). This floor will be gradually raised starting per 1st of January of 2022, the minimum capital requirements for banks will be gradually increased (from 50% to 72.5% of the Standardized Approach).

- 2023 : 50% of Standardized Approach

- 2024 : 55% of Standardized Approach

- 2025 : 60% of Standardized Approach

- 2026 : 65% of Standardized Approach

- 2027 : 70% of Standardized Approach

- 2028 : 72,5% of Standardized Approach

On top of that De Nederlandsche Bank (DNB) has decided to introduce a capital floor for mortgages only starting in 2022. If the outcome of the required capital of their internal models is lower than calculated by the Standardized Approach, banks have to upgrade their capital requirements to this (national) capital floor. The floor is introduced because the European System Risk Board (ESRB) recommended DNB and the Dutch government to do so, using as main argument the increased system risk in the Dutch housing market. The necessity to act on this increased system risk only in the banking industry is because of the

- reasoning that banks are more vulnerable for decreasing house prices than insurers and pension funds caused by their larger exposure to the Dutch house market and economy.

- Although banks also face other risk types, they are not allowed to take diversification between different risk types or portfolios into account but have to add up all individual required capitals. Additionally, no other allowances (i.e. loss absorbing capacity of taxes) are taken into account.

Insurance companies (Solvency II regime)

Under Solvency II, the available capital (“eligible own funds”) is defined based on an economic value or fair value basis. The required capital (“required SCR”) can be derived using the Standard Formula or using Internal Models. The conditions to apply an internal model are severe and only a limited amount of large insurance companies apply partial internal models (i.e. NN Group, Aegon and Achmea). The use of the Standard Formula is the most common in the market and is based on the aggregated outcome of capital requirements related to six different underlying risk modules[3]. Different levels of diversification are taken into account: both within the different risk modules as well as between different risk modules.

On top of this companies are – subject to the performance of a recoverability assessment – allowed to lower their capital requirement with a tax adjustment (the Loss Absorbing Capacity of Deferred Taxes or LACDT). Similar to banks, Internal Models are allowed to derive the capital requirements. The risks related to Mortgage loans are classified as Type 2 risk within the counterparty default risk module, and capital charges are based on a risk-weighted measure. The solvency capital requirement for counterparty default risk is calculated as 15% of the ‘loss given default’ (LGD). In case of residential mortgages, the LGD is defined as the value of the mortgage loan minus the maximum of 80% of the risk-adjusted value of the residential property, and the guarantee. The risk-adjusted value of the residential property equals 75% of the property’s market value.

The Solvency II framework does not contain additional liquidity buffer requirements or a required leverage ratio as prescribed within the Basel III framework.

Pension Funds (FTK regime)

The majority of pensions in the Netherlands are based on defined benefit schemes. The Pensions Act (“Pensioenwet”) contains safeguards designed to ensure that an agreed pension can actually be paid out. These safeguards are regulated by the FTK (“Financieel Toetsingskader”). The FTK states how the investments and liabilities (the future payments) of the pension funds have to be calculated on a fair value basis / economic value basis. Furthermore, the FTK specifies required buffer amounts derived on a value at risk approach based on an approach that can be considered as a rather simplistic version of the Solvency II framework.

The FTK capital requirements for Pension funds with respect to mortgage loans are rather straightforward. Unlike the Solvency II capital requirements for Insurance companies there is no relationship between the LTV of a mortgage and the required capital. Spread shocks are used on the cash flows of mortgages to calculate the required capital. For mortgages which fall into the AA bucket, this shock amounts to 80 bps. How this translates into capital requirements depends on the timing of the cash flows (i.e. duration of the mortgage). Assuming a duration for the mortgage portfolio of 9.3 years, the capital requirements amount to roughly 4.5% without diversification. Similar to insurance companies, pension funds are also allowed to take diversification into account under the FTK regime. The expected diversification benefit is around 40%.

[3] Market risk, counterparty default risk, life underwriting risk, non-life underwriting risk, health underwriting risk, operational risk

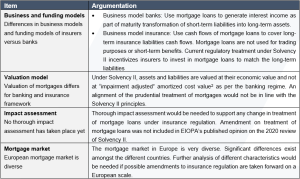

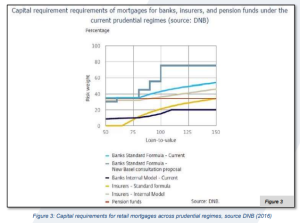

Comparison mortgage capital requirements based on DNB paper in 2016

DNB paper in 2016 can lead to the conclusion that prudential regimes are inconsistent or unfair

The initiative of the EC to align the prudential regulation of mortgage loans between banking regulation and insurance regulation is driven by an ESRB (European Systemic Risk Board) paper. The ESRB paper shows a comparison of mortgage capital requirements for banks, insurers and pension funds under current prudential regimes and is used by the ESRB to justify recommendations to adjust the Solvency II capital requirements for mortgage loans. The comparison is derived based on a 2016 paper of DNB[4] and is summarized below.

[4] De Nederlandsche Bank – Kredietmarkten in beweging – November 2016

In its 2016 paper, DNB compares the following capital requirements:

-

- Banks (Basel III regime): The total capital requirement for credit risk arising from mortgage loans. The capital requirement of banks mainly consists of credit risk. No capital requirement arises from the liability side, so diversification plays a rather limited role for banks when compared to insurers.

and

-

- Insurers and Pension funds (Solvency II / FTK regime): The counterparty default risk resulting from investments in mortgage loans is added to a material Life Risk capital and Market Risk capital also taking into account the impact of diversification and allowances for tax. DNB only shows the marginal contribution to the Total Capital Requirement (SCR) from investments in mortgages and this is much lower than the Standalone capital requirement for counterparty default risk. To compare apples with apples, the Standalone capital requirement for counterparty default risk should be compared to the capital requirement for mortgages under the Basel regime.

Based on the above reasoning, it can be concluded that the comparison shown by DNB in its 2016 paper cannot simply be regarded as a fair and equal comparison. Unlike banks, insurers must maintain a substantial capital requirement for Market (mismatch) risks and Life risks arising from the long term liabilities on the liability side of the balance sheet. The impact of diversification which DNB shows in their graph makes clear what the marginal capital requirement is, if mortgages are added. Without this context it seems that the capital requirements for mortgages within the insurance regime are much lower than within the banking regime.

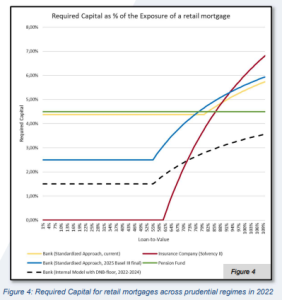

True comparison mortgage capital requirements in different prudential regimes

True comparison of capital requirements for mortgage loans under different prudential regimes requires to compare “apples with apples”

Given the discussion in the previous section we believe that for a more true comparison one would have to compare the Basel III capital requirement (banks) with the standalone capital requirement under mortgage loans under Solvency II (insurance companies). This section shows this more true comparison of the mortgage capital requirements under different prudential regimes on the basis of an “apples with apples comparison”[5].

- Banks: mortgage loan capital requirements under Basel III requirements

- The yellow line displays the capital requirements for banks under the current Standardized Approach

- The blue line displays the capital requirements if Basel III ‘Final’ is enforced in 2025.

- However the large players on the Dutch mortgage market all have internal models that since the beginning of 2022 are floored by DNB, these capital requirements are shown by the black dotted line.

- Insurers: mortgage loan capital requirements under Solvency II standard formula (red line)

- Pension funds: mortgage loan capital requirements under FTK capital requirements (green line)

[5] From a consistency point of view, diversification with other risks has not been taken into account. Furthermore, any loss absorbing impact of future taxes is ignored.

Based on the above results, it can be concluded that the capital requirements for a comparable residential mortgage loan can vary between the different prudential frameworks. Depending on the duration of the cash flows Pension Funds seems to have the (relative) highest required capital for mortgages, before diversification[6]. Insurance companies are facing the lowest capital requirements, even before diversification.

This in itself is not surprising, certainly in view of various statements about this by regulators and financial literature on this. It is relevant, however, that the differences are relatively small in the LTV range of 75%-100% where the biggest exposure of newly originated mortgage loans is concentrated.

Another point of attention is that the mortgage capital requirements for insurance companies under Solvency II decrease very sharply for LTV values of 80% or lower. For LTV values below 60%, the capital requirements even become nihil. This is not realistic, since this would imply that there is no credit risk at all, while in reality there is material credit risk exposure even for low LTV loans.

It is important to note that the capital requirements from the graph above cannot simply be compared. After all, at insurers and pension funds, capital charges are applied to the fair value of the mortgage loan, while at banks the exposure value as defined via the Capital Directive is leading[7]. In practice this valuation approach means that mortgages are valued according to amortized cost.

For the average portfolios of mortgages on the balance sheets of insurers, it appears that the valuation on an economic basis at the end of 2021 results in a 5%-10% higher valuation than when a valuation on a nominal or amortized cost basis is assumed. After the increase in interest rates in 2022 the economic value is around or even below the amortized cost value.

Other points of interest are for example that under the Basel III regime (banks), partial guarantees from central governments, regional governments and local authorities (i.e. “NHG guarantees”) are exempt from the calculations of the (floored) capital requirements. Where this is not the case under Solvency II (insurers) and FTK (pension funds); they are forced to ignore the NHG guarantee.

[6] Assuming a duration for the mortgage portfolio of 9.3 years, the capital requirements amount to roughly 4.5% without diversification.

[7] Banks should determine the Exposure At Default. Mostly the exposure at default moment is higher than at the current exposure.

Further analysis based on actual figures

Analysis of real case results for some banks and insurers reveals interesting insights

In this section we show the actual results for banks and insurers from the market based on the situation at the end of 2021.

In order to achieve a level playing field, it is relevant to note that banks and insurers currently apply different criteria to express the level of capitalization. It is possible to calculate comparable ratios for both types of settings. This provides interesting insights.

It is customary for banks to express the required capital in Risk Weighted Assets and the Capital Requirement is then converted by dividing the Risk Weighted Assets by 12.5. This is due to the original Basel I capital requirements that the total capital (equity capital used to cover the required capital) of a bank must be equal to 8% of the total assets. For some assets, the underlying risk exposure was lower and therefore lower risk weights are ultimately assigned, so that the risk weighted assets – which serve as the basis for determining the capital requirements – are usually lower than the total balance sheet assets.

An important measure to express the degree of capitalization of a bank is the total capital ratio. The capital adequacy ratio is calculated by dividing a bank’s total capital by its risk-weighted assets. Currently, more attention is paid to the Common Equity Tier 1 ratio (CET1 ratio) to evaluate the capitalization of banks. A bank’s tier 1 capital ratio is calculated by dividing its tier 1 capital by its total risk-weighted assets.

It is common for insurers to assess capitalization on the basis of the solvency ratio. This is derived as the insurer’s total eligible capital by its required capital. This measure can be derived by multiplying the insurer’s total capital ratio by 8%. Although insurers are also increasingly making use of subordinated loans that do not qualify as unrestricted tier 1 capital, the internal capitalization targets at insurers are still mainly based on their total eligible capital, in contrast to banks.

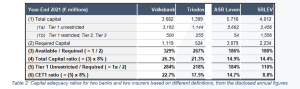

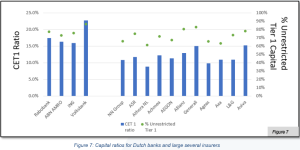

To illustrate the differences between the two types of institutions, we show below the derivations of the capitalization for four institutions that are supervised by DNB:

- Bank entity 1: Volkbank N.V. (“Volksbank”)

- Bank entity 2: Triodos Bank N.V. (“Triodos”)

- Insurance entity 1: ASR Levensverzekering N.V. (“ASR Leven”)

- Insurance entity 2: SRLEV N.V. (“SRLEV”)

For Volksbank, the capital requirements of mortgage loans are calculated using an Advanced Internal Ratings Based (IRB) Approach. In the case of Triodos, the Standardized approach is applied.

ASR Leven is a solo life insurance entity which is part of ASR Netherlands and SRLEV is also a solo life insurance entity which is part of Athora Netherlands Group. Both entities use the Standard Formula to determine their capital requirements.

The derivation of the capital requirements for these four institutions can easily be derived from public disclosures and is set out in the table below. This clearly shows the differences in definition between banks and insurers to express their capital requirements.

Some relevant remarks in relation to the figures above are set out below:

- Capital requirement for insurers is after allowance for diversification and loss absorbing impact of taxes. For the calculation of the capital requirements of the two insurers, it can be seen that diversification and tax benefits are included. This is not the case with the banks, since the total capital requirement simply follows from the sum of the capital requirement of the underlying risk types.

- Low capital requirement Volksbank related to use of an internal model. For Volksbank, the capital requirement expressed as a % of the total assets is rather low at 1.7% compared to the other institutions shown. This is partly due to the use of an internal model for credit risk. The capital requirement is expected to increase materially as a result of the application of the minimum floor that DNB introduced for internal models for retail mortgages from 2022.

- Mortgage capital requirements less relevant for insurance companies. It can be seen for both ASR Leven and SRLEV that the capital requirements for mortgage loans play only a limited role in relation to the total capital requirement. The reason for this is that only a limited part of the investments is invested in mortgage loans and that other risks such as interest rate risk, credit spread risk and life underwriting risk are much more important risks.

- Differences in capital requirement insurers due to different ALM and reinsurance strategies. For ASR Life and SRLEV it appears that the capital requirement for ASR Life is relatively higher than for SRLEV. This can have several reasons. In any case, ASR has been involved in a rerisking process for some time with the aim of improving the risk profile of the investments, so that the market risk profile of ASR Life is expected to be higher than that of SRLEV. In addition, part of the longevity risk exposure of SRLEV has been reinsured. Both insurers use the Standard Formula so there is no difference in capital measurement approach.

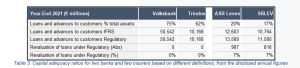

The level of capitalization for these four institutions is shown in the table below. As stated above, different definitions for capitalization are used by banks and insurers. From the point of view of comparability, we have derived both definitions in the table below and we also provide insight into how the different capital ratios relate to each other.

The eligible capital held at the two banks is relatively higher than at the two insurers if the measures are examined according to the same definition. In the next section, we examine to what extent this also applies to the entire sector.

As noted in the previous section, the valuation of mortgage loans that is applied to banks for the purpose of determining eligible capital and required capital is equal to the valuation as it applies on the IFRS balance sheet.

For the two insurers examined, it can be seen that the valuation of mortgage loans underlying Solvency II eligible capital and Solvency II required capital is approximately 7% higher than the valuation on the IFRS balance sheet at year-end 2021. It is also relevant that the market value of mortgage Loans have decreased in value in 2021. While at the end of 2021 there was an equity surplus of 7% for both insurers, at the end of 2020 this was equal to 12%-13% for the two insurers. In the course of 2022, the value of mortgage loans declined further due to increasing interest rates.

Level of capitalization

Level of capitalization compared to regulatory requirement is higher for banks compared to insurers

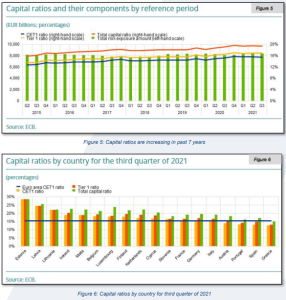

The previous section discussed the level of capitalization of two random banks. The ECB also publishes these statistics for the entire European banking sector. This shows that the Common Equity Tier 1 (CET1) ratio has increased approximately to 15.5% towards year-end 2021. This is summarized in the figure below.

To make a comparison between the banking industry and the insurance industry, we made a comparison between the level of capitalization for four large Dutch banks compared to several large European insurance groups.

The level of capitalization is expressed on the basis of the Common Equity Tier 1 (CET1) ratio. We also provided insight into the extent to which the total eligible capital consists of unrestricted tier 1 capital.

The above figures show that the large Dutch banks use unrestricted tier 1 capital to the same extent as the large European insurance groups. In almost all cases, the percentage of unrestricted tier 1 capital lies in a 70%-80% range of the total eligible capital.

The CET1 ratio held for European banks is approximately 15.5%. The large Dutch banks are slightly above this (CET1 ratio of 16% or higher), but it must be taken into account that these large banks all use internal models and after the application of the minimum floor for retail mortgages in the Netherlands per 2022, the CET1 ratio is expected to decrease and may come more in line with the European average. Compared to European banks, most of the major European insurance groups surveyed have a relatively lower implied CET1 ratio of 10%-13%.

It can be concluded from this that the level of capitalization in relation to regulatory capital is on average higher for European banks than for European insurers.

So even if the European Commission manage to equalize the regulatory required capital for mortgage credit risk, the question is whether the overall objective will be successful in creating a level playing field.

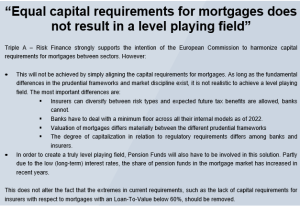

Equal capital requirements for mortgages does not result in a level playing field

Although Triple A – Risk Finance supports the intention of the European Commission to strive for an level playing field and equalizing the capital requirements for mortgages. By proposing the latter (only), the goal will not yet be reached.

Arbitration based on supervisory rules between sectors is not desirable. It disrupts free market forces and exposes financial institutions to risks as a result of (possible) changes in regulations. This causes unnecessary instability in the system and goes against the purpose of prudential supervision. That is why Triple A – Risk Finance strongly supports the intention of the European Commission to harmonize capital requirements for mortgages between sectors. However:

- This will not be achieved by simply aligning the capital requirements for mortgages. As long as the fundamental differences in the supervisory framework exist, it is not realistic to achieve a level playing field. The most important differences are:

- Insurers can diversify between risk types and expected future tax benefits are allowed, banks cannot.

- Banks have to deal with a minimum floor across all their internal models as of 2022.

- Valuation of mortgages differs materially between the different prudential frameworks

- The degree of capitalization in relation to regulatory requirements differs among banks and insurers.

This results in quite significant capital levels between banks and insurers, which are not solved by “just” changing the capital requirements for mortgages.

- In order to create a true level playing field, Pension Funds will also have to be involved in this solution. Partly due to the low (long-term) interest rates, they have served an increasing share of the mortgage market in recent years.

This does not alter the fact that the extremes in the current regulation, such as the lack of capital requirements for insurers for mortgages with an LTV < 60% should be removed. On top of that :

- With the introduction of the national capital floor in the Netherlands since 2022 and the decreasing benefit of internal models under the regime of Basel III “finalizing post crisis reforms” over the total credit risk, the question arises how interesting it is for banks to continue developing an (approved) internal model for mortgages? Credit risk models will always be used for internal business purposes, but the costs of maintaining a supervisory approved model might in that case outweigh the benefits.

- Regulations at banks and insurers were amended years ago in such a way that the capital buffers reflect the actual risks. This is only the case to a limited extent for pension funds and it would be a big step forward to introduce such a framework in this market as well, independent of the mortgage capitalization.

- In the past decade there has been a trend among insurers to invest more in High Yield (spread of risks, search for yield) due to market valuation, but at the same time this will now have a significant impact on P&L. Banks are not facing this P&L impact because mortgages are valued on book value. For future ALM decisions, not only yield considerations and capital requirements should play a role, but so should the P&L effects.

Publicaties

Alle publicaties

Alle publicaties

Thom Peters

Reservering vanuit actuarieel perspectief en de impact van negatieve rekenrentes

In dit artikel bespreken Cees en Nico de totstandkoming van de voorzieningen van een verzekeraar, de uitdagingen hierbij voor letselschadeclaims en de impact van negatieve rekenrentes.

Frank van Houdt

Scenariobedragen leiden tot betere pensioneringskeuzes

Een goede pensioneringskeuze vereist goed inzicht in de uitkomsten. Deelnemers waarderen scenario’s hierbij en deze beïnvloeden het keuzegedrag dan ook significant. In dit artikel toont Triple A – Risk Finance collega Wouter Otten de meerwaarde aan van URM-scenario’s voor pensioneringskeuzes.

Marten de Boer

DNB past uitgangspunten uniforme scenarioset aan

In de scenarioset van DNB was een te hoge lange termijn renteverwachting opgenomen, wat leidt tot communicatie van te optimistische scenariobedragen. DNB heeft deze aangepast en Triple A – Risk Finance licht hier de effecten toe voor de verschillende regelingen.-

-

Wilt u meer informatie of een afspraak maken?

Neemt u dan contact op met Tom Veerman

Neem contact met mij op

© 2026 AAA Riskfinance. Alle rechten voorbehouden.